Critical minerals for tax credit buyers

Share

.svg)

.svg)

.svg)

Want to explore more conversations like this?

View all blogs

Executive summary: The §45X critical minerals tax credit pays domestic producers and refiners 10% of production cost (2.5% for metallurgical coal) for producing any of 50 statutorily defined critical minerals plus metallurgical coal. It is one of the largest and most actively traded categories in the transferable tax credit market.

Introduction

Critical minerals tax credits are transferable §45X advanced manufacturing production tax credit (PTC) generated by companies that extract or process eligible critical minerals in the United States. For tax credit buyers, these credits can offer attractive pricing, large transaction volumes, and relatively straightforward diligence compared to some other transferable tax credit opportunities.

Congress made critical minerals eligible for the §45X PTC to encourage domestic production of critical minerals that are essential to energy technologies, advanced manufacturing, and national security. Because the United States remains heavily dependent on foreign supply chains for many critical minerals, the credit is designed to incentivize domestic extraction, processing, and refining capacity.

For tax credit buyers, critical mineral tax credits can offer large transaction sizes, competitive pricing, and limited recapture risk. This guide covers how §45X critical mineral tax credits are generated, how they are priced, the risks buyers should evaluate, and current market trends.

Key takeaways for tax credit buyers:

- The §45X eligible-mineral list is established in statute and includes lithium, cobalt, graphite, nickel, manganese, aluminum, and rare earths, among others. Metallurgical coal also qualifies, at 2.5% of production cost.

- The credit equals 10% of production cost for most minerals (2.5% for metallurgical coal), with no per-unit cap. The October 2024 final regulations allow inclusion of certain material and extraction costs, plus §263A indirect costs.

- Minerals must meet specific purity thresholds — typically 99% by mass, with aluminum required at 99.9%.

- §45X advanced manufacturing PTCs (inclusive of critical minerals) were the second-largest segment of the 2025 tax credit market — approximately $9 billion in transaction volume, or 25.5% of total volume.

- §45X pricing has historically reached a high-water mark of around $0.96 per dollar of credit for the largest investment-grade deals, with deals in the low-to-mid $0.90s common.

- Under the OBBB, the critical minerals credit phases down — 75% of value in 2031, 50% in 2032, 25% in 2033 — and is eliminated for credits produced in 2034 and later.

- §45X is a production tax credit with no recapture risk to buyers, which contributes to its strong pricing in the transferable tax credit market.

What are critical minerals?

The Energy Act of 2020 directed the US Geological Service (USGS) to produce and update a list of critical minerals based on three criteria:

- The mineral must be essential to US economic or national security.

- The mineral’s supply chain must be vulnerable to disruption.

- The mineral must be essential to the production of energy, technology, or systems used for national defense.

The USGS updated its list of critical minerals in 2022 and released a revised version in November 2025. This 2025 list covers 60 minerals, including many that are foundational in clean energy components.

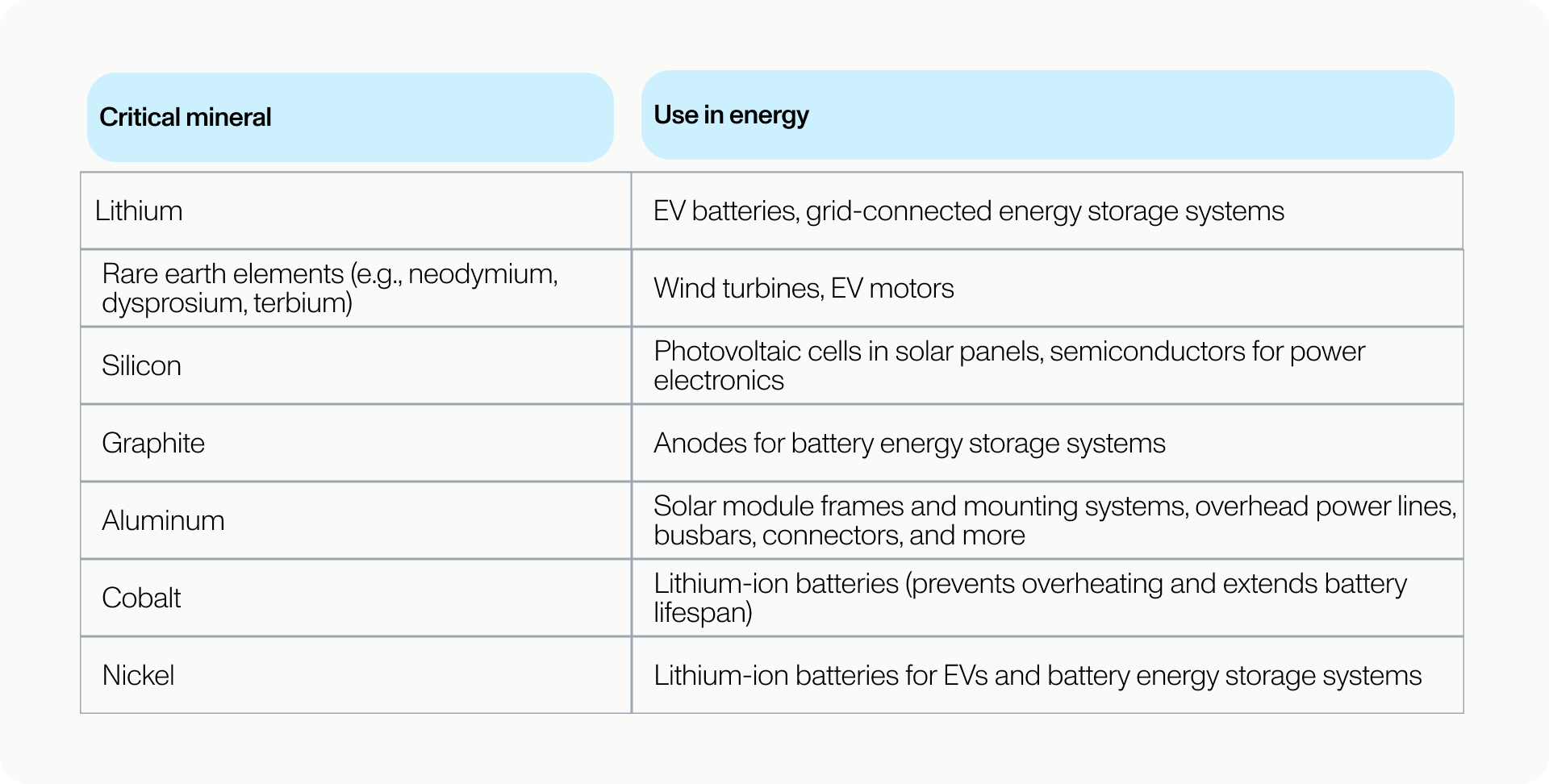

Select critical minerals and their use in energy

Critical minerals play a central role in clean energy manufacturing and in the production of many high-tech goods. In a report published in January 2025, the USGS noted that the US is 100% reliant on imports for 12 critical minerals, especially from China. For rare earths, a subset of critical minerals that are specifically valuable for their conductive and magnetic properties, China controls 60% of global production and 90% of refining and processing capacity.

Reshoring supply chains and increasing domestic production of critical minerals is a core focus of the §45X tax credit.

Critical minerals tax credits incentivize a domestic supply chain

The §45X advanced manufacturing PTC incentivizes domestic extraction, processing, and manufacturing of critical minerals in the US. The §45X credits are transferable, which allows smaller companies spearheading new mineral extraction and refining technologies to unlock needed capital for innovation and expansion by selling the credits to third parties.

To qualify for §45X tax credits, eligible materials must meet IRS-defined purity thresholds. Most qualifying minerals must reach at least 99% purity by mass. Some minerals require higher thresholds. For example, aluminum must be at least 99.9% pure by mass.

Taxpayers claiming the credit must maintain certificates of analysis documenting mineral purity.

How is the value of the §45X tax credit for critical minerals is calculated?

The §45X critical minerals PTC is calculated as 10.0% (or 2.5% in the case of metallurgical coal) of the production cost of a domestically produced or processed critical mineral sold to a third party in the US. In addition to the direct costs of production, there are several important rules regarding how companies can assess the value of their tax credits.

Acquisition costs

In draft guidance published in November 2023, the Internal Revenue Service (IRS) prohibited including mineral acquisition costs in calculating the value of the §45X critical mineral tax credit. The final guidance released in October 2024 allows the inclusion of certain material costs, including extraction costs, for applicable critical minerals and electrode active materials. This change addresses concerns raised by stakeholders about the exclusion of material costs, acknowledging their contribution to value-added production.

Indirect costs

The final IRS guidance permits companies to include indirect costs according to §263A in the calculation of the §45X credit value. Indirect business costs are company expenses not directly related to the extraction or processing of critical minerals. They include employee benefits and payroll costs, depreciation or amortization of equipment, and taxes and insurance related to production activities.

Direct pay eligibility

Section 45X credits may qualify for elective pay, also known as direct pay, which allows eligible taxpayers to receive cash payments directly from the IRS instead of transferring credits to a third-party buyer.

However, many manufacturers and mining companies choose to sell transferable tax credits because transfer transactions can generate cash proceeds faster than IRS refund processing timelines.

Did OBBB change the expiration of the §45X critical mineral tax credit?

The Inflation Reduction Act initially provided a permanent §45X tax credit for eligible critical minerals. However, the OBBB introduced a phaseout schedule for critical minerals beginning in 2031. For eligible critical minerals (excluding metallurgical coal), the credit is reduced to:

- 75% of the full credit value for minerals produced in 2031

- 50% of the full credit value for minerals produced in 2032

- 25% of the full credit value for minerals produced in 2033

The credit is scheduled to be eliminated for critical minerals produced in 2034 and later.

OBBB also added metallurgical coal as an eligible critical mineral, but only through 2029 and at a reduced credit rate.

How are §45X credits transacting in the market?

According to Crux’s State of Clean Energy Finance: 2025 Market Intelligence Report, advanced manufacturing PTCs, including critical minerals tax credits, sustained robust demand in 2025. Approximately $9.0 billion in §45X credits transacted over the full year, accounting for 25.5% of total transferable tax credit market volume. Advanced manufacturing was the second-largest tax credit category by market share.

This proportion decreased slightly from 30.9% in 2024, likely due to heightened uncertainty around new prohibited foreign entity requirements for §45X credits passed in the One Big Beautiful Bill (OBBB), which caused some buyers and developers to pause and recalibrate. Crux estimates that an additional $3–5 billion of eligible §45X credits did not transact in 2025 and may shift into the 2026 market.

Observed §45X pricing in 2025 became more differentiated across deal size, and pricing generally declined after the passage of the OBBB. In 1H2025, deals transacted at prices that were relatively consistent with 2024, especially for large deals. In 2H2025, overall pricing declined. Manufacturers that sat on the sidelines in 2025 are coming back to the market in early 2026 with premium price expectations, and Crux expects pricing for 2025 §45X credits sold in 2026 to rebound toward or above 1H2025 levels.

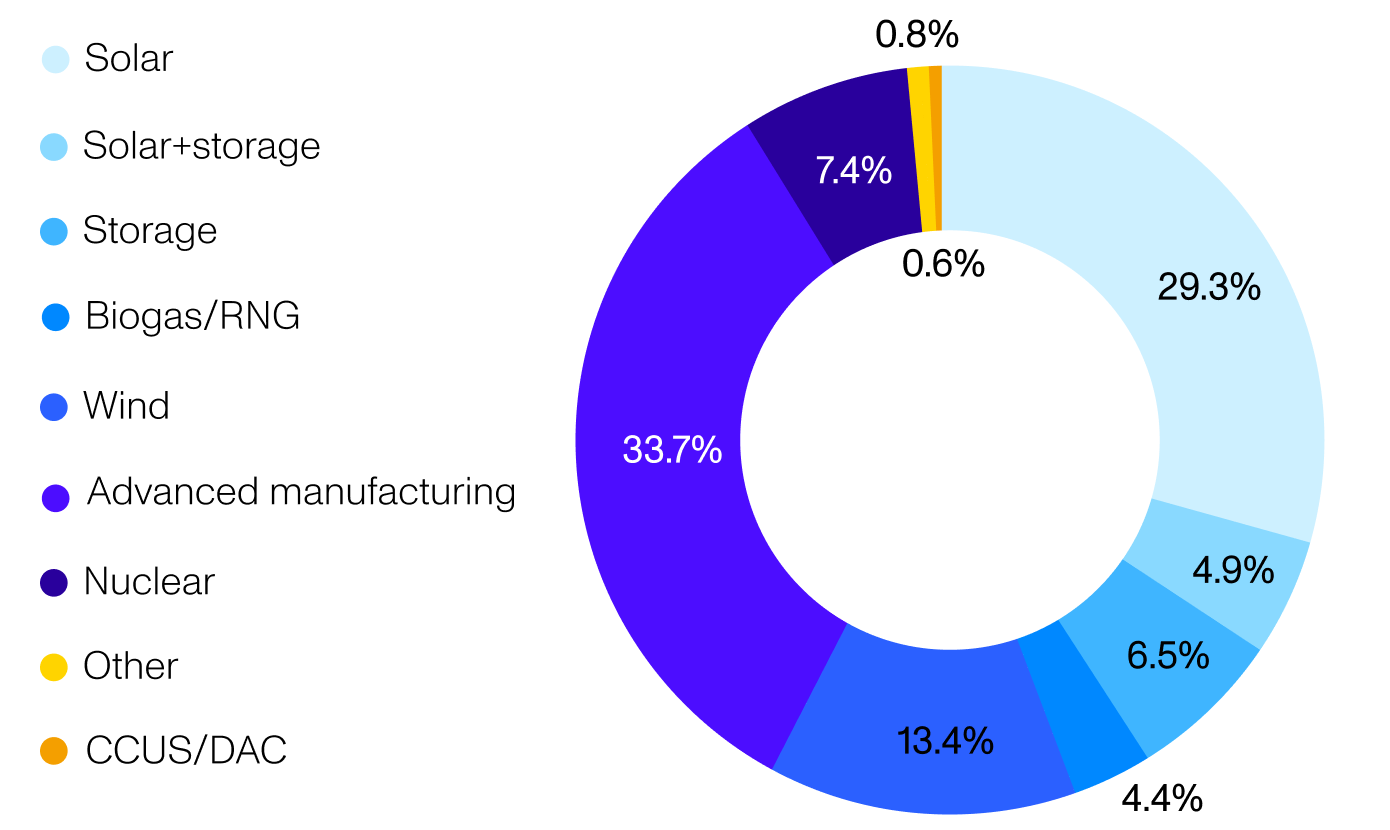

Market composition, 2024 full year (by dollar value, 2024 tax credits)

Deals were most commonly transacted as spot or short-term strip purchases (usually two to three years), and transactions ranged in value from approximately $20 million to more than $1 billion.

The benefits of critical minerals credits to buyers

Section 45X credits offer several benefits for tax credit buyers and investors:

- Simplicity: Once a miner or manufacturer substantiates the critical mineral tax credit and its value, the transactions are straightforward.

- No risk of recapture: Production tax credits such as the critical minerals credit are not subject to recapture, or the risk that some part of the tax credit may be reclaimed. There is no risk to the buyer because sellers must demonstrate that they have produced and sold a certain volume of critical minerals before the tax credit is generated.

- Large volume of tax credits: Section 45X deals are more likely to involve a large volume of credits and competitive pricing relative to other large electric-generating tax credits.

Popularity drives strong prices for critical minerals tax credits

Demand for advanced manufacturing PTCs rose throughout 2024 and has remained strong in early 2025. About 35% of commercial bids placed on Crux in the first quarter of 2025 were for advanced manufacturing tax credits. Crux has observed that demand consistently outstrips supply for these credits.

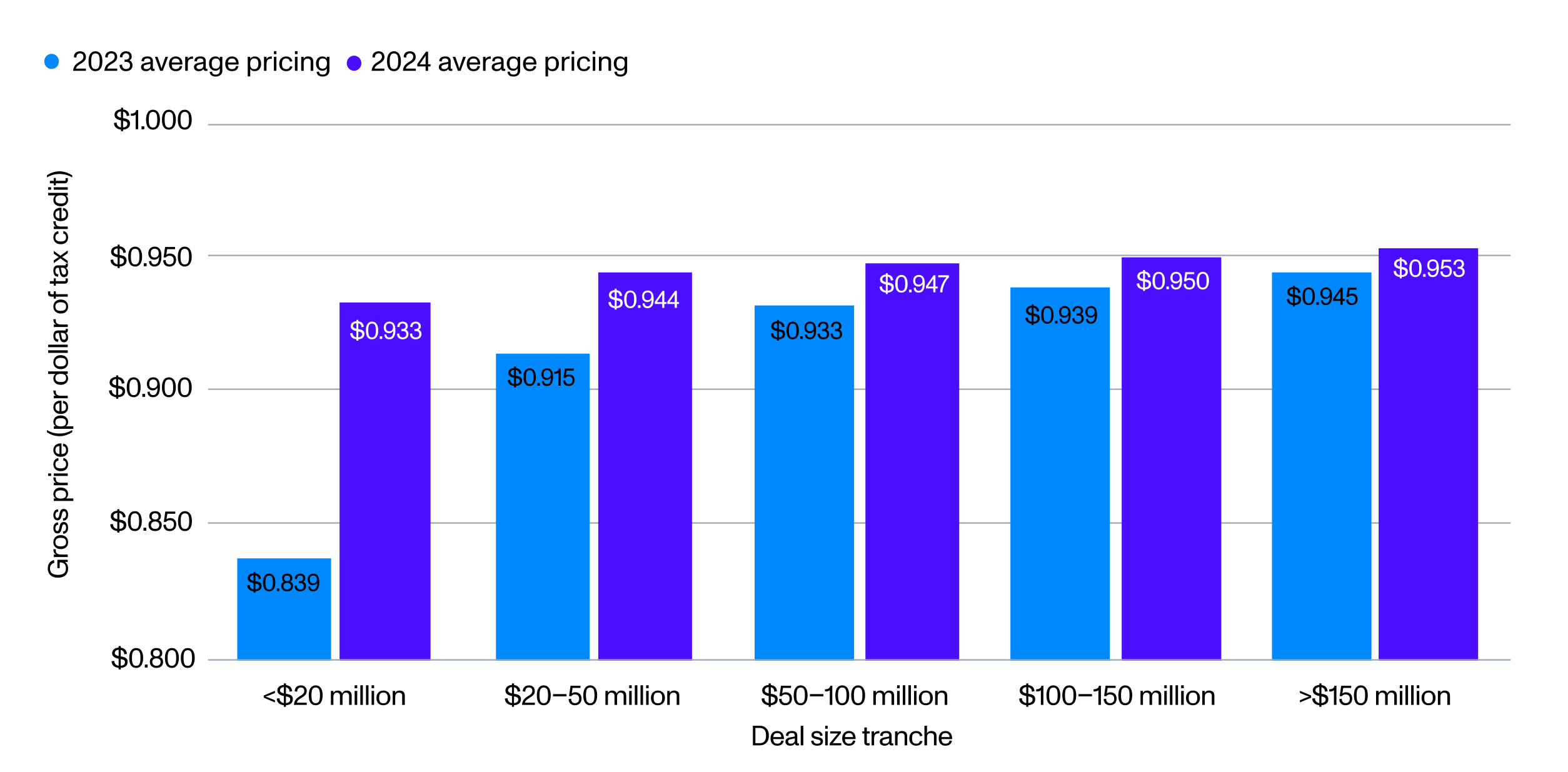

Pricing for these credits is consistently in the range of $0.92–0.96 at the highest end of the deal curve.

Advanced manufacturing PTC pricing by deal size tranche, year over year

Insurance and parent company indemnification

Insurance and parent guarantees remain important credit-enhancement tools in §45X transferable tax credit transactions.

According to Crux’s market data: About half of advanced manufacturing deals included either insurance or a parent guarantee. That figure has declined since 2023 as the credit has become more established. Average insurance cost was 3.7% of total transaction value, Average coverage level was around 120%. The amount of insurance coverage is typically reported as a percentage of the notional deal value — coverage over 100% reflects a gross up, typically covering penalties, interest, and taxes. Coverage below 100% can provide credit support for the seller’s parent indemnities.

Glossary: Critical Minerals

- Critical minerals Minerals designated by the USGS as essential to economic security, energy technologies, or national defense.

- Section 45X tax credit A federal advanced manufacturing production tax credit created by the Inflation Reduction Act.

- Transferable tax credit A tax credit that can be sold to another taxpayer for cash.

- Direct pay A mechanism allowing eligible taxpayers to receive cash refunds directly from the IRS.

Further reading

For a broader overview of advanced manufacturing credits, see our essential guide to advanced manufacturing tax credits.

To learn more about the market for advanced manufacturing tax credits in 2025 and understand Crux’s predictions for 2026, download our 2025 market intelligence report.

To understand how prohibited foreign entity guidance impacts §45X tax credits, see our breakdown of initial Treasury guidance on prohibited foreign entity rules.

Share